In this article:

- Weigh the interest vs. invest equation carefully

- Factor in unexpected events

- Get a second opinion

The question of whether to put extra cash against your mortgage to pay it off early has two distinct components: emotional and rational. On an emotional level, your home represents so much more than the return you might get from it — it’s where you raise a family and create memories.

On a purely rational level, a home is like buying an investment: You take out a loan, buy a home, make payments and hope it appreciates in value. But, as we were reminded in the first half of 2022, investment markets don’t always go up. And neither do home values.

Setting emotions and market unpredictability aside, here are three considerations to keep in mind if you’re thinking of paying off your mortgage early.

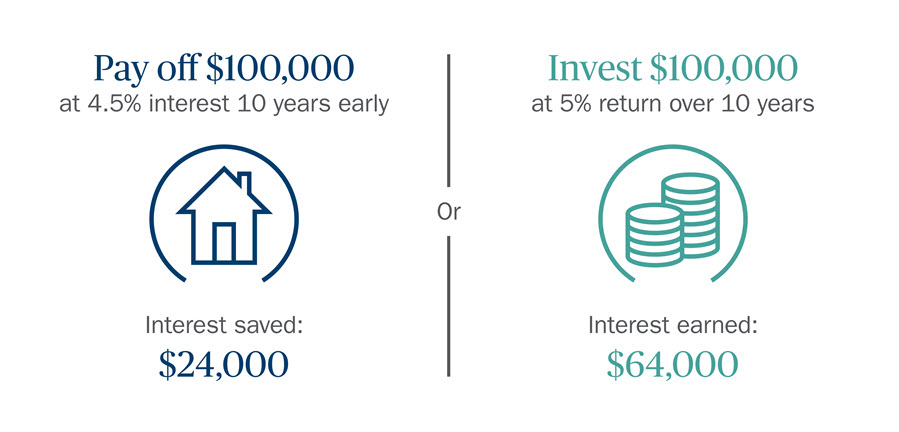

1. Weigh the interest vs. invest equation carefully

The return on paying off your mortgage early — either through regular extra monthly payments or by occasional lump sums — is the amount of money that would have been paid in interest. What you don’t know is the return you would have gotten on the money if you invested it instead.

That question often proves to be an irresistible siren call to invest for homeowners. Many people calculate based on their risk tolerance and portfolio allocation, assuming they can earn more back from the market than they pay out in mortgage interest and save with tax deductions. This means that younger investors — who have more time to benefit from market returns — may choose to invest the money they would have used to make extra house payments.

That said, interest rates aren’t as much of a make-or-break factor as homeowners may think when deciding whether to pay off the mortgage or invest. When mortgage interest rates are low, expected returns in the stock market can be even lower. This is particularly true for people nearing retirement, who tend to reduce their exposure to risk by investing in fixed income rather than equity products.

Pay off home or invest 100k?1

2. Factor in unexpected events

In theory, a homeowner’s cash flow is improved by saving money instead of spending more on extra mortgage payments, which enables them to better deal with unexpected expenses such as a health event. But if those expenses are severe enough to drain your cash reserves, you get hit with a double whammy: Savings are depleted, and your home could be at risk because you can’t afford mortgage payments.

Before even considering paying off your mortgage, make sure to fund savings and retirement accounts and pay off other higher-interest loans. If you’ve paid off your home, consider setting up a home equity line of credit as soon as possible in case you need liquidity down the road. In an emergency, you could access the equity in your home.

3. Get a second opinion

With so many factors at play, talk with us before making any mortgage-related decisions.

We can work with your tax professional to help you evaluate how retaining or paying off your mortgage will affect your tax situation — a component that is often more impactful than homeowners may realize.

We can also help you explore other scenarios based on income, savings, lifestyle, expenses and risk tolerance.