Noah Funderburk, Director of Securitized Credit, US Portfolio Manager – Amundi

3/18/2024

For the first time in many years, savers can earn a reasonable return in cash. But how long can these compelling rates last?

Historically, the answer is not very long. Here’s why:

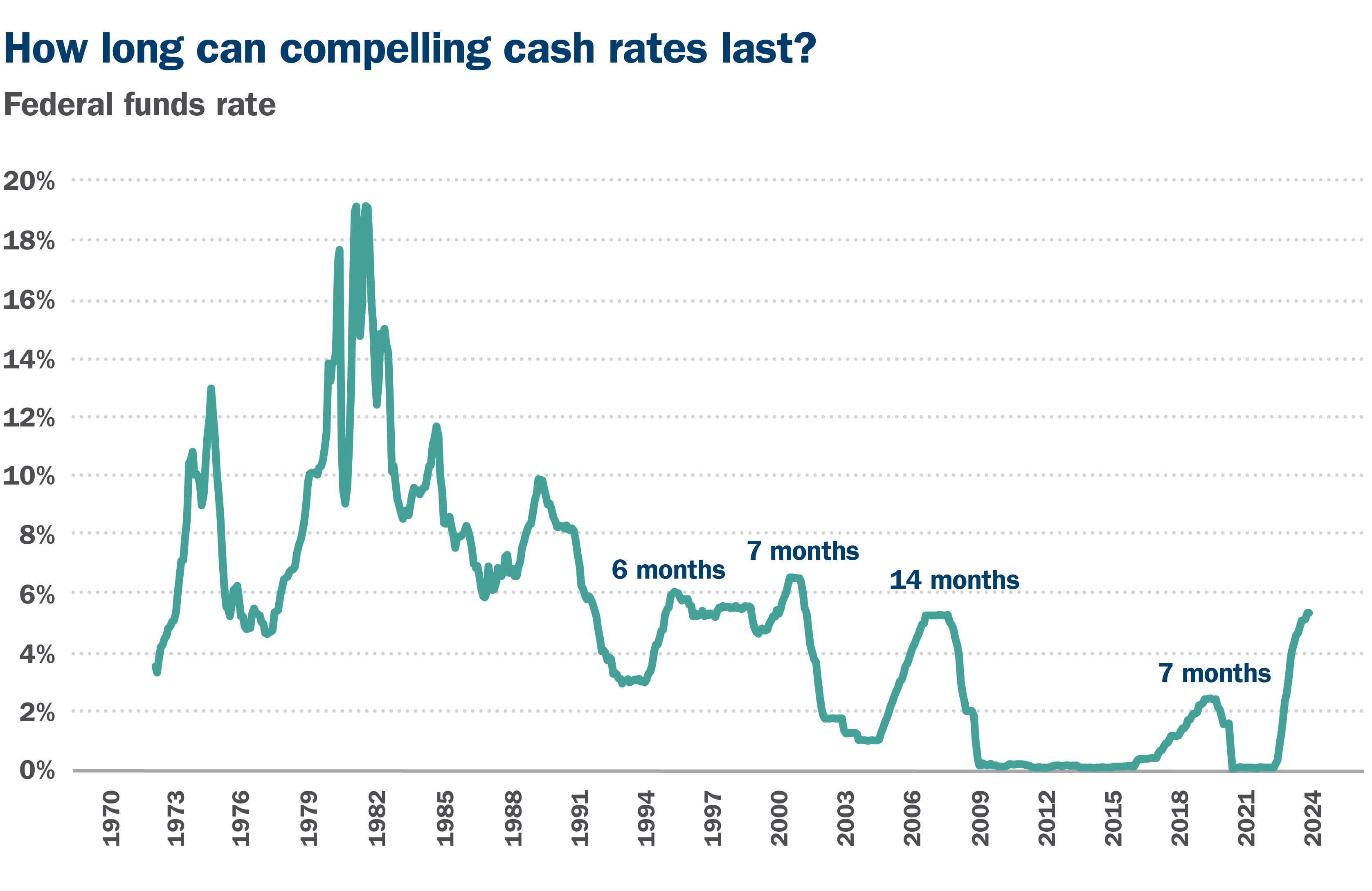

The Fed pausing rate hikes is telling

After a nearly three-year selloff in the U.S. bond market, with periods of positive correlation between equities and bonds, it’s understandable that investors have found comfort in cash in recent years.

But the period of elevated cash returns may be coming to an end soon, if past Federal Reserve activity is any indication.

In every rate hike cycle since the 1970s, the Fed has “paused at the peak” of the federal funds rate for a matter of months, not years. Furthermore, once the Fed starts cutting the funds rate, cash rates can move hundreds of basis points lower in a short period of time.

Source: Bloomberg, Oct. 16, 2023. Federal funds effective rate

For illustrative purposes only.

The reinvestment risk of cash

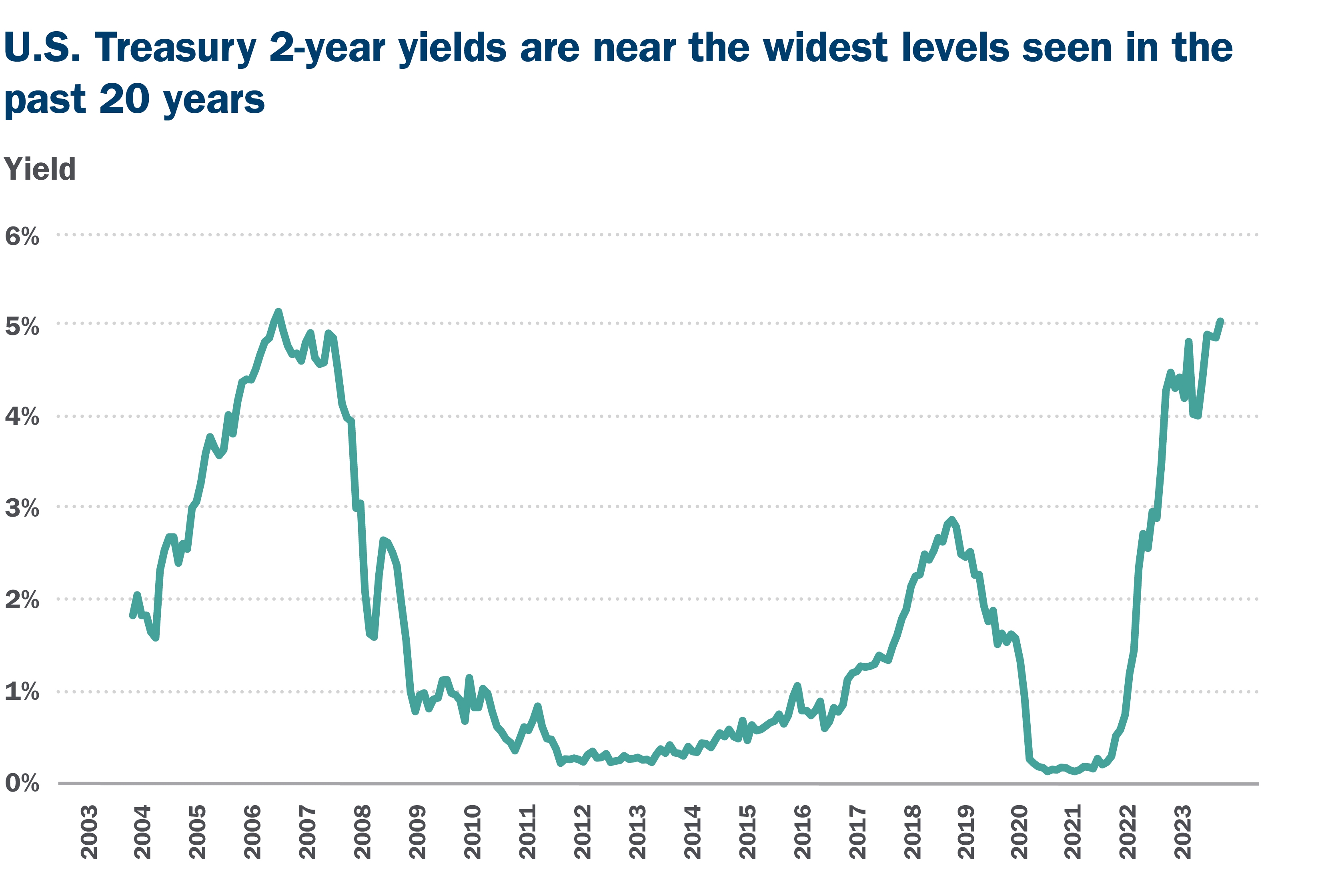

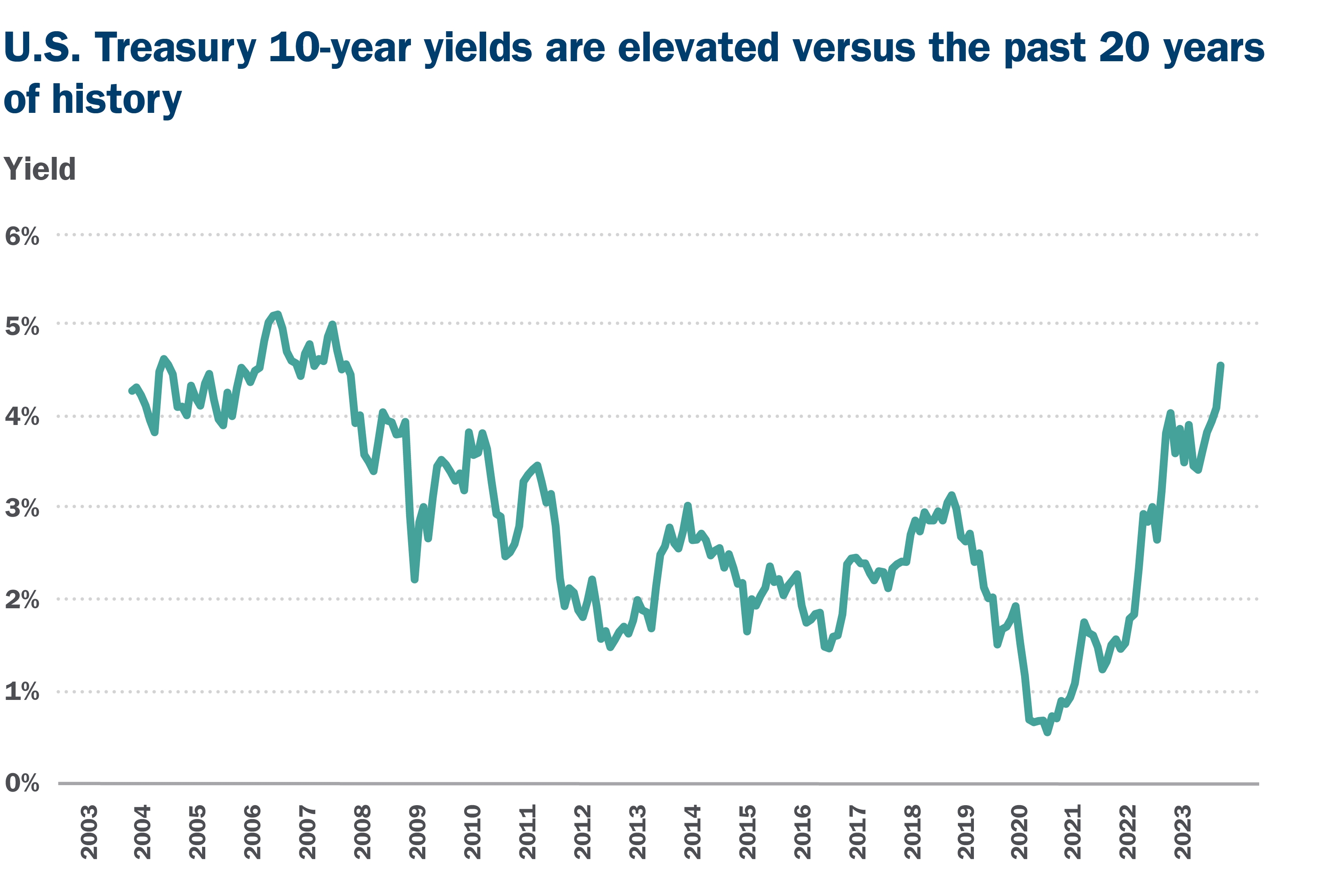

This history suggests cash investors today may be taking on substantial reinvestment risk at a time when interest rates in fixed income appear unusually attractive versus history (see the charts below). How many other asset classes are nearly the cheapest they have been in 20 years? What investment decisions would be made if the same could be said today about the equity market or housing market? Of course, such valuations do not arrive without reason, and recent bond market volatility may continue in the near term. Bottom line: Against the interest rate risk inherent in most fixed income securities, investors should consider the reinvestment risk that is inherent in cash.

Source: Bloomberg, Oct. 16, 2023. Notably, the currently elevated rate levels are not explained by inflation. The U.S. Treasury Inflation Protected Securities (TIPS) market likewise indicates real yields are attractive versus history (not pictured). For illustrative purposes only and not guaranteed. Past performance is not a guarantee of future results.

Source: Bloomberg, Oct. 16, 2023. Notably, the currently elevated rate levels are not explained by inflation. The U.S. Treasury Inflation Protected Securities (TIPS) market likewise indicates real yields are attractive versus history (not pictured). For illustrative purposes only and not guaranteed. Past performance is not a guarantee of future results.

Bottom line

While cash interest rates may be relatively high today, those elevated levels may not last very long. For investors whose objectives can be measured in months or years rather than days, we believe today’s historically elevated interest rates may call for allocating at a point on the yield curve that controls for volatility risk without ignoring reinvestment risk. Moving into longer-maturity fixed income securities may help investors lock in today’s attractive income levels before they disappear.

Weigh your options with the help of a financial advisor

Connect with your Ameriprise financial advisor to review your cash investments and fixed income allocation.