This illustration is hypothetical and is not meant to represent any specific investment or imply any guarantee.

3. Invest for the long term

It may be tempting to try and time the market — buy and sell investments based on what you believe the market is going to do in the future — but you risk losing quite a bit of money, over time. During volatility, the worst days in the market are often closely followed by some very good days. When you take money out of the market on a downturn, you may miss the subsequent upswing and recovery in prices.

Time is on the side of the investor and a buy-and-hold strategy usually produces better results in the long term.

We can help you create a personalized investment plan that looks at both inflation and your long-term goals, to help you retire with more confidence.

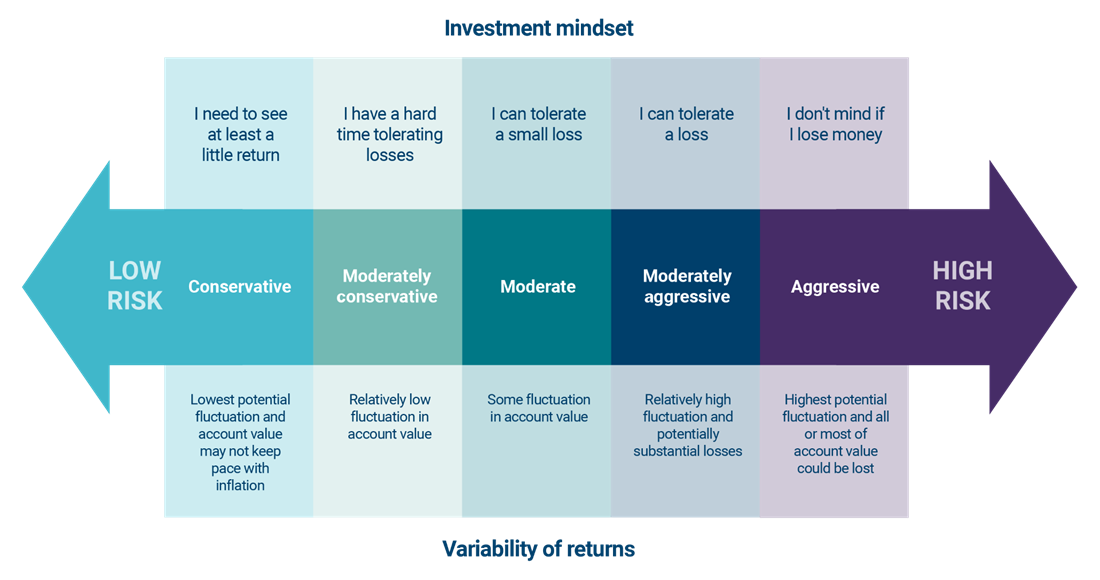

4. Take your risk tolerance level into account

What are your goals for investing? Are you comfortable losing money if the stock market performs poorly or does any sort of investment loss make you nervous? These are the types of questions to think about and discuss with us to help gauge your tolerance for risk.

Investors with more time to recoup market losses may be more comfortable taking risks. However, as you near retirement or if you’re already retired, you may want to adjust your risk tolerance to make sure your investments are consistent with your goals.

Once you’ve determined how much risk you’re willing to accept and what your investing time frame is, we can help you allocate assets and diversify your portfolio accordingly.

Take our risk tolerance quiz

You can determine your risk tolerance for investing by answering a few questions.

Take the quiz