Anthony Saglimbene, Chief Market Strategist – Ameriprise Financial

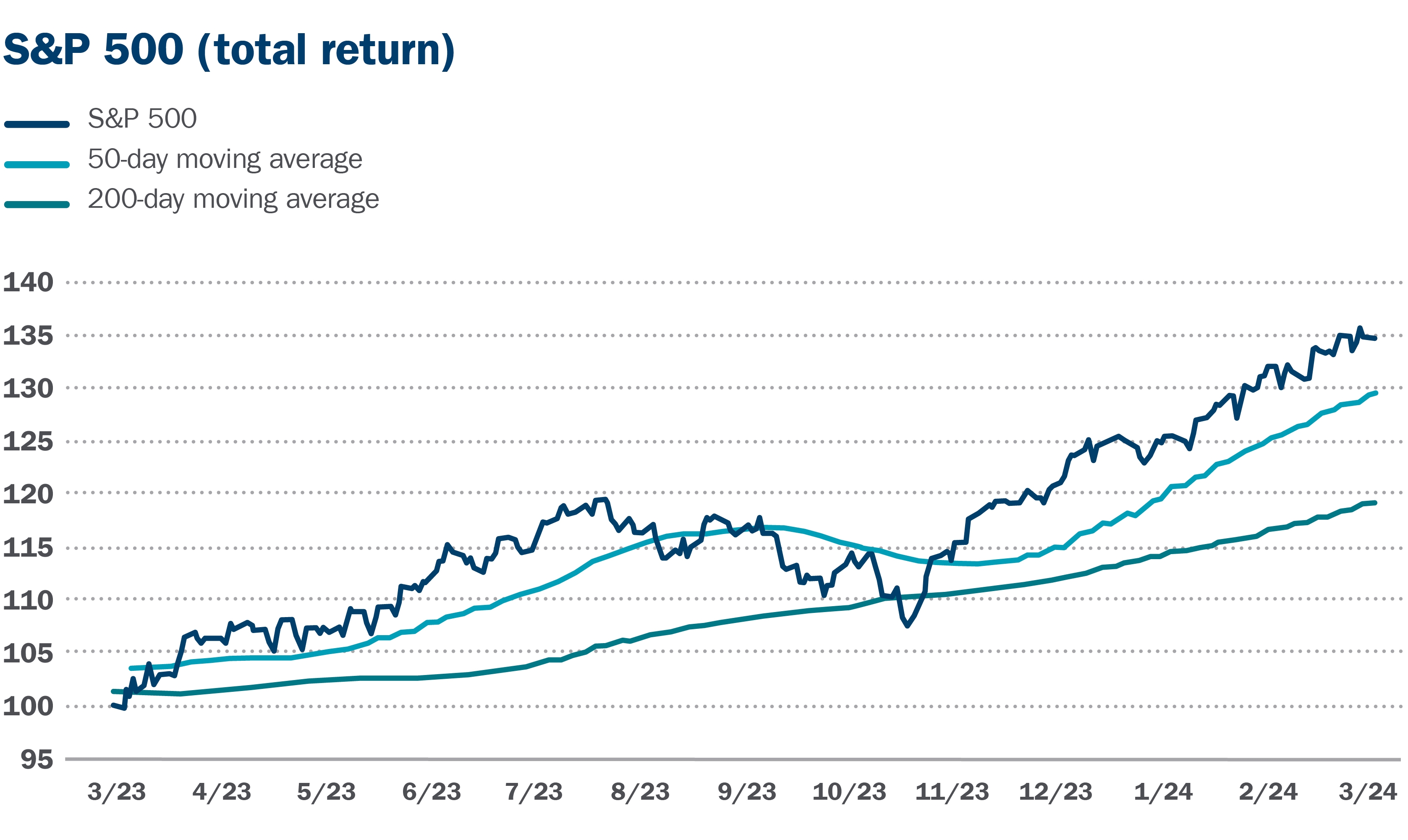

Stocks started 2024 with a big bang. Major U.S. averages spent the first two months of the year accelerating higher, finishing February higher for the fourth consecutive month. Through the end of February, both the S&P 500 Index and NASDAQ Composite were higher by over +7.0% year to date — and that’s after the S&P 500 gained +26% and the NASDAQ shot higher by +45% in 2023.

Overall, the stock market’s run over the past four months has been impressive. But how much longer can this rally last? Here’s what the bulls and bears are saying:

Source: FactSet and American Enterprise Investment Services, Inc. Data as of March 11, 2024.

This example is shown for illustrative purposes only and is not guaranteed. It is not possible to invest directly in an index. Past performance is not a guarantee of future results.

The bull case

In our view, there has been a meaningful change in the overall tone of the stock market over recent months, one that is far more positive than just six months ago. This bullish narrative can be attributed to a few key dynamics:

- Strong profit gains across Big Tech: The phenomenon — coupled with investor expectations that profit growth will likely improve across other areas of the economy as the year progresses — has been a key driver of stocks.

- Growing investor confidence in supportive fundamentals: The expectation that the U.S. economy will remain on a stable growth trend, while consumer and business spending remain positive, is becoming a prevailing belief among a broader constituent of market participants.

- Falling inflation: Notably, we see inflation dropping close to the Federal Reserve’s 2.0% target by the end of the year.

- The market’s expectations around lower interest rates: To some extent, stocks continue to make new highs because an increasing number of market participants believe the Federal Reserve will start to cut interest rates by the back half of the year.

Bottom line: A growing economy, inflation moving back to the Fed’s 2.0% target over time, low unemployment, resilient consumers/businesses, lower interest rates by year-end and accelerating corporate earnings are all dynamics that could be very supportive for higher stock prices throughout the year, in our view.

The bear case

Stocks have come a long way fast, with the S&P 500 up roughly +25% from the October lows. And bearish investors may point to the following points to support their case that the stock market tone could shift in 2024:

- Stocks have not seen a meaningful correction in over four months: In our view, stocks are likely overdue for some consolidation or even an extended period of modest declines. In some respects, investors are likely incorporating the bullish factors we outlined above into stock prices today and moving ahead of incoming data that supports the soft-landing narrative. Thus, the risk that some of these factors come in less positively than expected could temporarily disrupt the upward momentum in stock prices for a period. Historically, the market typically sees a drawdown period of at least 5%-10% intra-year.

- Unforeseen economic changes could pose a risk to interest rate policy — and asset prices: The central narrative behind Fed rate cuts this year continues to assume solid economic fundamentals, which allows policymakers the luxury to gradually normalize monetary policy on their terms. Any changes in the economic environment that cause the Fed to leave rates higher for longer than most expect, unexpectedly raise rates or aggressively cut rates, are risks not only to the soft-landing narrative but to asset prices more broadly. While this is not our expectation for the year, it remains possible, which creates some outside risk of increased volatility throughout the year.

- Presidential election years come with their own unique challenges: Presidential election years typically see stock volatility rise in the summer months before normalizing quickly in early November and after election results are known.

- Profit/performance leadership across the S&P 500 is narrow: This is another concern for the bears, however, we believe investors should discount this worry if economic fundamentals remain sound. We expect the market rally to broaden to an increasing number of industries, sectors and asset classes as the year progresses. Improved performance in materials, industrials and small-cap stocks during February may be an early sign of this point. Further, outside of a handful of mega-cap tech stocks, equity valuations are not nearly as stretched, particularly if we are right about the fundamental backdrop for this year.

Bottom line: We believe market and economic conditions at the start of the year are supportive of higher equity prices, even with the run higher in the S&P 500 this year. How much more depends on whether profit trends over the year unfold as we expect and if economic growth remains resilient in the face of still-elevated interest rates.

Why staying on the sidelines may be a misstep

When the market reaches new highs, it can be tempting to turn cautious with your investing. However, after setting a new high for the first time in more than a year, history suggests the S&P 500 Index will likely continue to see above-average returns in the following year. In our view, investors should maintain a cautiously optimistic outlook for equities, but also be prepared for bumps in the road should this year see some unexpected twists and turns.

Take advantage of the bull market

A well-diversified investment strategy can help investors participate in the current bull market while managing portfolio risks should the market run into unexpected headwinds. Reach out to your Ameriprise financial advisor if you have questions about how your investment portfolio is built to take advantage of opportunities in both bear and bull markets.