Choosing your retirement health care coverage is an important decision — but it can feel complicated. As you learn about the Medicare enrollment process, here are three things to keep in mind about the federal health insurance program:

What is Medicare?

Medicare is a nationwide federal health insurance program for people ages 65 and older, or those with qualifying illnesses and disabilities. This four-part program is designed to support each individual’s retirement health care needs, hospital services, outpatient services, prescription drug costs or a combination of them.

1. Medicare doesn’t cover all health care costs

Medicare is a valuable program for many retirees, but it wasn’t designed to cover health care expenses in full. While doctor visits and routine medical and emergency services are covered, Medicare doesn’t cover vision, hearing or dental — and there is limited coverage for nursing home and other long-term care options. In some cases, premiums and copays for covered services may become significant.

Here are the four parts of Medicare and what they cover:

- Part A: Hospital Insurance

Covers the care you receive while an inpatient at a hospital or skilled nursing facility.

- Part B: Medical Insurance

Covers doctor visits, routine medical services such as flu shots, and emergency medical services.

- Part C: Medicare Advantage

Provided by private insurance companies and offers Medicare Part A and Part B coverage, usually with additional benefits, including vision and dental coverage. Medicare Advantage plans often have more barriers to care and are more restrictive on provider access.

- Part D: Prescription Drug Plan (PDP)

Provides prescription drug coverage through plans administered by private insurers.

2. Missing the initial Medicare enrollment window may result in penalties

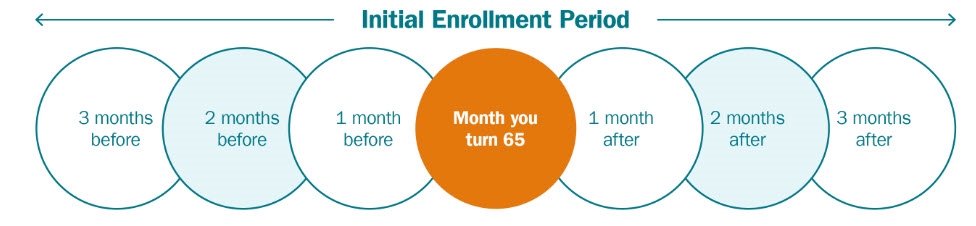

Initial Enrollment Period: This period is a seven-month window that begins three months before you turn 65. If you sign up for Original Medicare, the initial enrollment for Medigap, known as your Medigap Open Enrollment, starts six months after initial enrollment in Part B.

If you don’t enroll during this initial period, you may face penalties for late enrollment. The Medicare program doesn’t send reminders.

If you are still working at age 65 and have employer-sponsored insurance, you may be able to enroll late in Medicare without penalty. Review the details of your situation carefully, and keep in mind that COBRA coverage does not exempt you from the penalty.

3. Your income prior to enrollment will affect how much you pay

Your income is a primary factor in how much you will pay for Medicare premiums. In general, the higher your income two years prior to enrollment, the more you will pay for Medicare premiums. Your premiums will also be higher if you haven’t paid into the Medicare system for a designated period of time.

In the years before retirement, it’s important to be aware of how your income could impact your Medicare prices. If you’re near the threshold, we can help identify strategies to reduce your modified adjusted gross income.

If you currently have Medicare coverage and your income goes down because of a life-changing event — marriage, divorce or death of a spouse, for example — you can contact the Social Security Administration to request a reduction of your Medicare premium.

Retire more confidently with the help of your financial advisor

Planning for health care in retirement can help you be better prepared to handle the expected and unexpected costs — and Medicare is a significant part of that planning.

If you don’t know where to start, we will help you understand the financial aspects of retirement health care and provide personalized advice based on your financial goals and unique situation. Our “Understanding Medicare” guide can also help you navigate your retirement health care choices.

Download our Medicare guide

Choosing your retirement health coverage is an important decision that can be complicated. This guide will help you to understand Medicare and the choices available to you.