While many investments are designed to grow over extended periods of time, there may be occasions when there’s only a short window of time to reach a goal, such as saving for a down payment on a home. For circumstances like these, we have compiled some primary tips for short-term investing, to help you better prepare for your situation.

How to position investments for the short run

Your time horizon is the amount of time you need to invest to achieve a financial goal. Even within a period of three years or less, your specific time horizon can provide guidance on the types of assets to consider, as well as the appropriate levels of risk to take.

For example, a portfolio with easily accessible cash investments may be more suitable if you need the money in three months, while someone who doesn’t need the money for three years can consider a wider array of investment options.

If you have a short time horizon, consider these three pieces of short-term investment information:

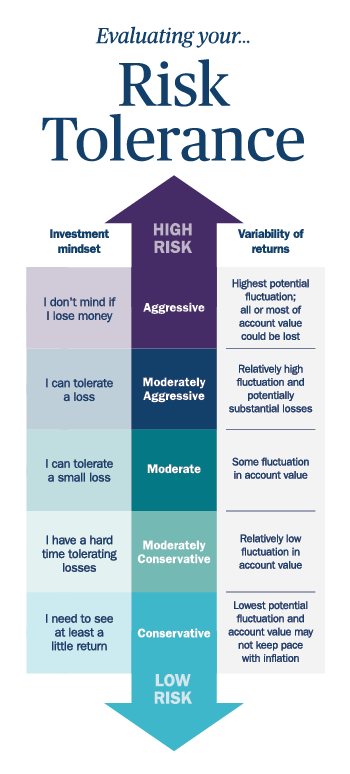

1. Determine your level of risk

Given such an abbreviated time period, it’s prudent to reduce the level of risk in an investment plan or portfolio. There typically isn’t enough time to recover from a loss that may occur if choosing higher risk assets such as stocks.

To illustrate, the stock market correction that occurred during the "dot.com" crash resulted in the S&P 500 Index dropping over 35% from 2000-2002 and it didn't fully rebound until 2006.

The short-term investment tip here is that, with a maximum of three years to invest, you should typically avoid investing in volatile assets.

Reducing the complexity of assets is another tip for short term investing. For example, non-U.S. assets are exposed to foreign currency movements, which add a layer of uncertainty that doesn’t generally affect U.S. assets.

2. Consider short-term instruments

Cash is a desirable asset for managing risk and liquidity and can be appropriate for very short horizons. Within the fixed-income universe, securities with less than three years to maturity, such as short-term bond funds, may be a good consideration.

3. Synchronize goal timing with your assets

If your specific time horizon is known (for example, three months, 12 months or three years), contemplate investing in products that generally match your investment timeline. Consider these examples:

- If you’re saving for a down payment on a house that’s due in six months, look for products such as short-term government bonds or AAA-rated corporate debt bonds.

- If you have a down payment on a purchased item due in six months, with the remainder of the purchase price to be paid in 12 months, then look for products with varying durations of six to 12 months, such as a laddered certificate of deposit (CD).

Make sure your investment strategy works for you

Once your plan has been determined, there may be additional factors to consider related to implementation depending on the products used. We can help customize a plan that aligns with your short-term goals while factoring in a broader view of your overall investment strategy.