Just about every part of life carries with it some generalized long-held beliefs. The economy is no different. But economic misperceptions can sometimes lead to misguided investment allocations or adversely impact investment decisions.

In this article, we examine some of those views and explain why they don’t always hold up when you take a closer look.

Myth #1: The American consumer is deep in debt

There have been many times in the past that it would have been appropriate to say consumers were “deep in debt.” Such broad statements today, however, can be misleading, and are not an accurate reflection of aggregate consumer finances.

In fact, since the Great Recession (2008-09), American consumers have been much more conservative with their finances and aggregate debt levels are quite low relative to incomes.

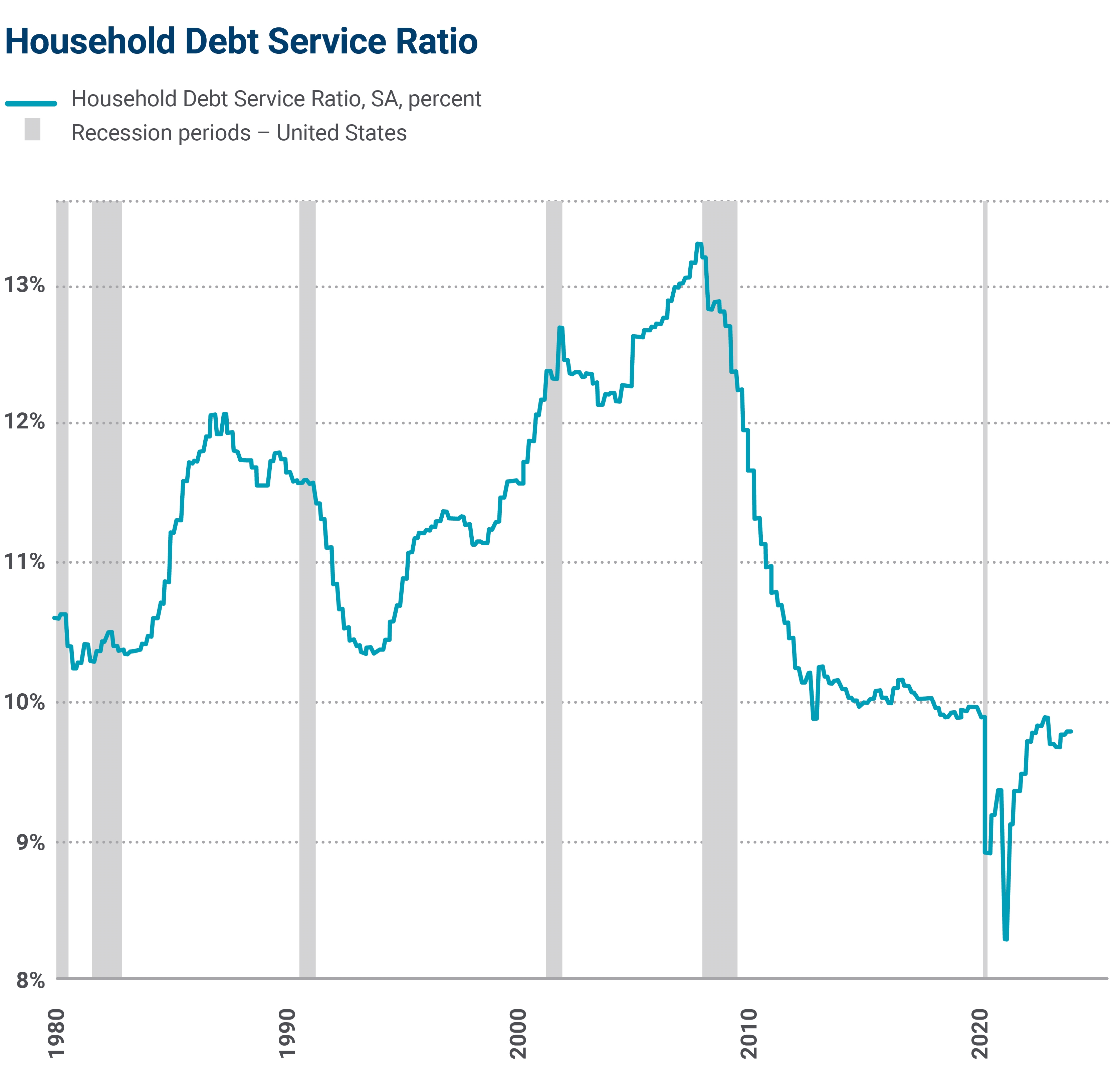

Just look at the Federal Reserve’s Household Debt Service Ratio (DSR). The measure looks at required consumer debt payments such as mortgages, credit cards, auto loans, student loans, bank loans and others, and measures these payments in what we believe is a logical manner — against consumer disposable income.

As seen in the chart below, the ratio was at an all-time high at the end of 2007, right as the Great Recession began. Conversely, it was at all all-time low (the series began in 1979) when the pandemic arrived in early 2020. Today, the ratio is still below its 2019-ending lows. Though not perfect, the measure offers a solid look at consumer spending power after all preexisting required payments are satisfied.

Source: Board of Governors of the Federal Reserve System (U.S.) Household Debt Service Payments as a Percent of Disposable Personal Income retrieved from FRED, Federal Reserve Bank of St. Louis; May 3, 2024.

Myth #2: Credit card spending is out of control

It’s been widely reported in recent months that credit card debt is at an all-time high. Indeed, at the end of 2023, the dollar value of credit card debt was over $1.1 trillion, according to the Federal Reserve.

However, these rising debt levels fail to take into account a longer-term trend: the widespread practice of using credit cards for everyday spending — and then paying off the balance every month. Consumers are increasingly turning to credit cards for their day-to-day spending, from groceries to gasoline, for convenience and to take advantage of perks like reward points.

Why does this matter? The Federal Reserve measures credit card debt in terms of its average monthly balance. As consumers increasingly use credit cards for convenience, the average monthly balance naturally grows, even if the bill is paid in full each month.

For example, if you start the month with a credit balance of zero, charge $2,000 on your card in a month, and then pay it off when due, you’d be justified to see yourself as having no credit card debt. However, your average balance for the period was $1,000, which is the number that gets factored into the measure.

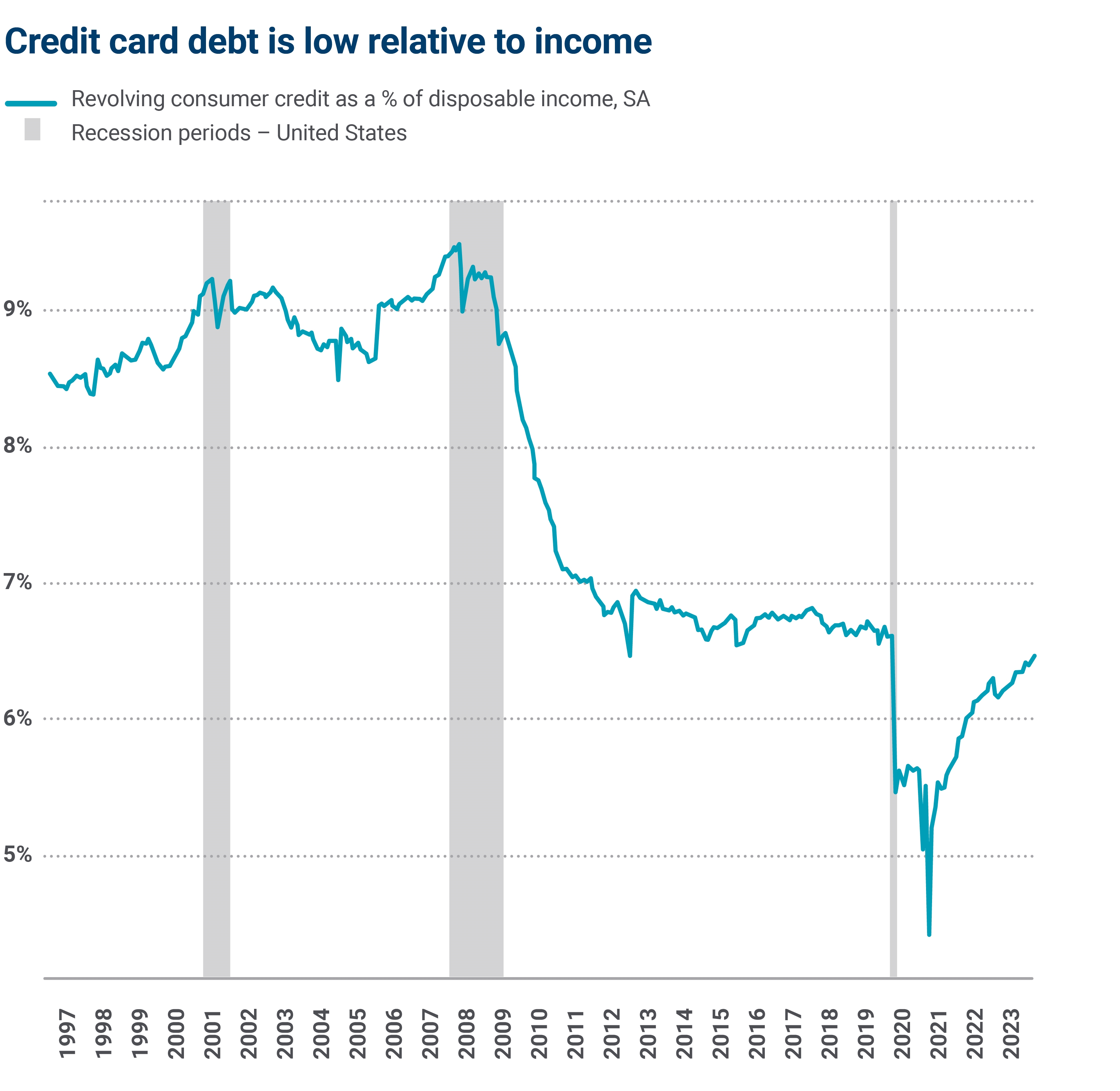

Source: Board of Governors of the Federal Reserve System (U.S.)

There is no way to strip-out this “convenience” factor, but we can look at credit card debt as a percentage of aggregate disposable consumer income, which is how the Household Debt Service Ratio is measured. If we look at credit card debt in this manner (see the above chart), there’s a drastically different story. Credit card debt as a percentage of disposable income is currently below its pre-pandemic levels and very low relative to its levels of the past 30 years.

Myth #3: The U.S. dollar is about to crash

Fear-based Internet advertisements that consistently predict a near-term collapse of the U.S. dollar have been around almost as long as the Internet itself. The ads typically appear as articles — and are often well written and quite convincing — but their primary goal is to scare people into subscribing to their newsletter.

The value of the dollar is often used because the factors that affect currency exchange rates can be challenging even for seasoned investment professionals to understand, let alone the average investor.

Additionally, those who write these newsletters know this topic can capture attention: Predicting an eminent dollar crash can be concerning given that people’s homes, investments and income are all valued in dollars. Often, some opaque issue related to the Federal Reserve is brought into the commentary to make it sound more legitimate. “Trigger dates” (e.g., ‘Our expert says the dollar will crash at the end of the month’) are also a common tactic to get readers to subscribe with urgency.

Currency values do indeed fluctuate, but they are also a “zero-sum” game since their value is directly relative to other currencies. As such, for a currency to go down in value, one or more other currencies must go up. Bottom line: Claims the U.S. dollar is on the verge of collapse are often baseless and are used to incite clicks and traffic.

We’re here to help you separate fact from fiction

There can be a lot of misleading noise and disinformation out there about the state of the U.S. economy. If there’s a particular narrative that’s concerning you, connect with your Ameriprise financial advisor. They can help you make sense of what’s fact and what’s fiction and help keep you on track with your investment strategy.