Get an overview of investments that can do well in an elevated interest rate environment, including potential risks and tradeoffs.

High interest rates can have a negative connotation with investors — especially in terms of their impact on the stock market and economy. When interest rates are high, so is the cost of borrowing, impacting everything from mortgages and credit cards to student loans.

But with increased rates also comes opportunity, particularly for short- and medium-term financial goals.

As you review the below investing opportunities, connect with us. We understand your financial situation and can make personalized asset allocation recommendations based on your risk tolerance, time horizon and financial goals.

Cash and cash equivalents

When interest rates rise, the popularity of cash investments also rise since investors can earn more competitive rates on these products.

Cash investments to consider

- Sweep accounts: By transferring unused funds into safer savings or investment options at the end of each business day, sweep accounts allow you to earn interest on money that you’re not actively saving or investing. However, rates may be lower given the daily accessibility to funds.

- Money market funds: Money market funds are mutual funds designed to provide liquidity and preservation of capital by investing exclusively in high-quality cash instruments (generally maturing in 60 days or less). Money market funds can offer higher yields than savings or checking accounts. However, they generally require waiting a day to access cash from a withdrawal and in the case of prime money market funds that invest in securities not backed by the U.S. government, could limit redemptions or charge liquidity fees during adverse market environments.

- Treasury bills: These short-term U.S. government debt obligations, backed by the U.S. Treasury Department, have a maturity of one year or less, from only a few days to a full 52 weeks. Since they’re considered a very safe investment, interest earned can sometimes be lower compared to the overall market.

- High-interest savings accounts: High-interest savings accounts are among the most conservative solutions. They offer immediate access to cash but generally do not offer the most competitive yields. These deposits, generally, have Federal Deposit Insurance Corporation (FDIC) insurance against loss.

Fixed income

Fixed income focuses on preservation of capital and income. This investment type pays out in fixed periodic installments and has the potential to provide a steady stream of income, but it can be challenging to sell and is easily influenced by interest rates, inflation and credit risks.

Fixed income opportunities to consider:

- Bonds and bond funds: Bonds are a type of debt security where the issuer generally promises to pay a specified rate of interest during the life of the bond and repay the face value of the bond (the principal) when it matures.

- When you buy individual bonds, you are loaning money to the bond issuer, which is typically a company or government agency. Unlike with stocks, you don’t obtain ownership stake in the company when you invest in bonds. Bonds have a maturity date when the obligation is due to be paid in full, and they usually offer fixed or variable interest payments.

- Bond funds benefit from diversified exposure to a basket of bond issuers and maturities, but are subject to market risk where the price when sold may be less than the purchase price.

- Investment certificates: This type of investment is an agreement between an investor and a financial institution. Certificates are designed to help build cash reserves and provide income to meet financial goals.

- Certificates of deposit (CDs): CDs are a type of savings account that offer higher-interest rates than regular savings accounts. Typically insured by the FDIC, CDs are a low-risk, fixed-term investment, which can be helpful if you’re saving with a specific goal in mind. If you need to access your investment before the maturity, you may forgo interest earned or face market risk.

Dividend-paying stocks

Certain companies return a portion of their profits to shareholders in the form of dividends. When you purchase stocks from these firms, you may receive quarterly payments from the company based on its net income and dividend policy.

If you choose to invest in dividend-paying stocks, you can potentially profit from any appreciation of the stock itself, and also earn money through distributions made to investors. Of course, all stocks are subject to market risk where the price when sold may be less than when purchased, which makes these a riskier overall investment. Additionally, dividend payments are not guaranteed and the amount can vary.

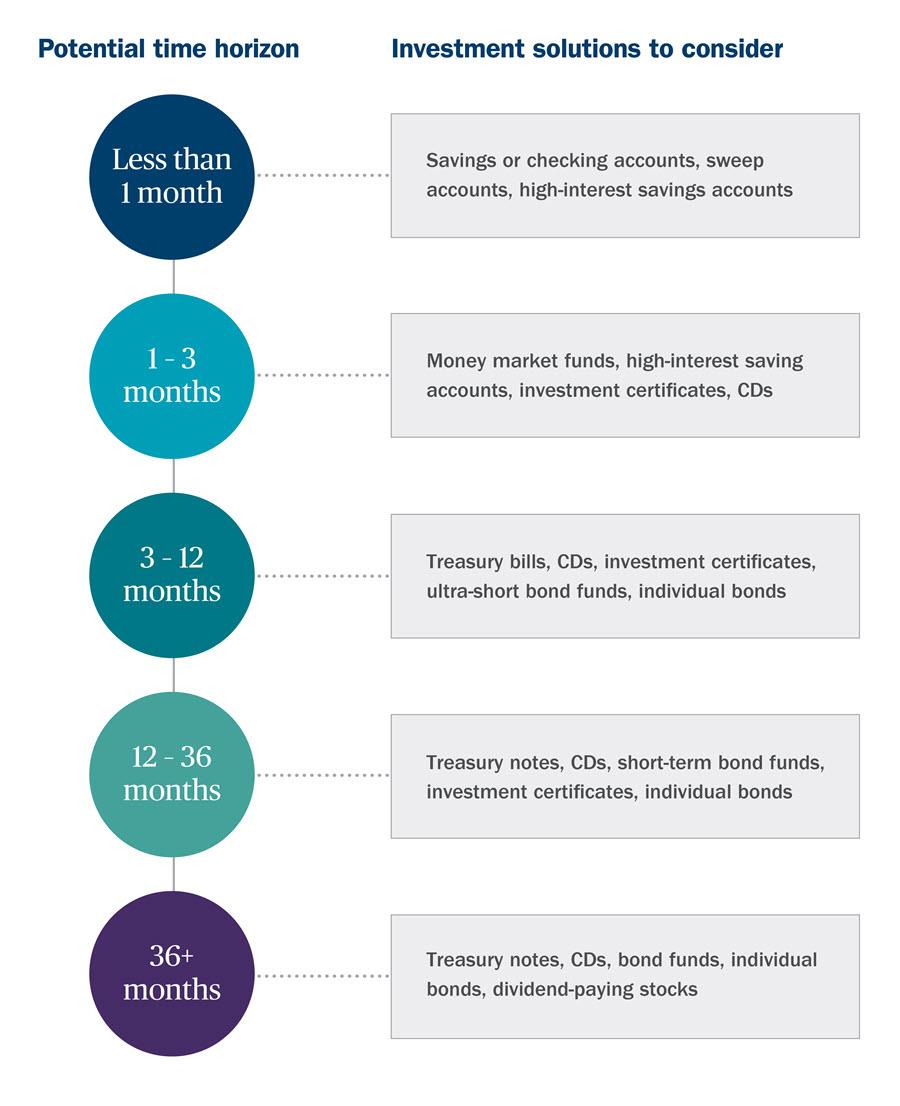

How time horizon fits into the equation

As you evaluate your options, consider your financial goals and time horizon, how soon the investment reaches maturity and how easily you’ll be able to access your capital, which is known as liquidity.

We’re here to help you understand your options

If you’re interested in discussing any of the above opportunities — let’s connect. We’ll review how these investments may fit into your overall strategy, considering your risk tolerance, time horizon and the level of liquidity you need to feel comfortable and secure in your current lifestyle.