Robert M. Almeida, Portfolio Manager and Global Investment Strategist – MFS Investment Management

There’s a surprising pattern in financial markets that, on the surface, appears counterintuitive: Everyday investors buy stocks when they are expensive and sell when they are inexpensive.

This “buy high, sell low” behavior may seem illogical, but it makes sense when viewed through the lens of human nature and our biological programming. However, if this cycle continues, future equity market returns could be more muted than investors expect.

Below, we explain what drives these tendencies and share practical ways to stay disciplined when markets test your instincts.

How biology drives the capital cycle in markets

All species are genetically programmed with a reward system designed for survival. Our brains are hardwired to seek pleasure and avoid pain. For example, a ripe strawberry tastes good and elicits a positive chemical response which encourages us to find and eat more. Conversely, things that are harmful tend to disgust and repel.

This same biological programming drives the capital cycle in financial markets:

Positive or outsized returns: When an economy, sector, industry or specific financial asset delivers outsized returns, it “tastes good,” triggering a powerful, dopamine-driven impulse to invest more capital into it.

Negative returns: Conversely, negative returns trigger an aversion response and the impulse to flee.

Boom-and-bust cycle: These dynamics create a self-reinforcing cycle of overinvestment in high-return areas and underinvestment in low-return ones, ultimately leading to the booms and busts that define economic and market history.

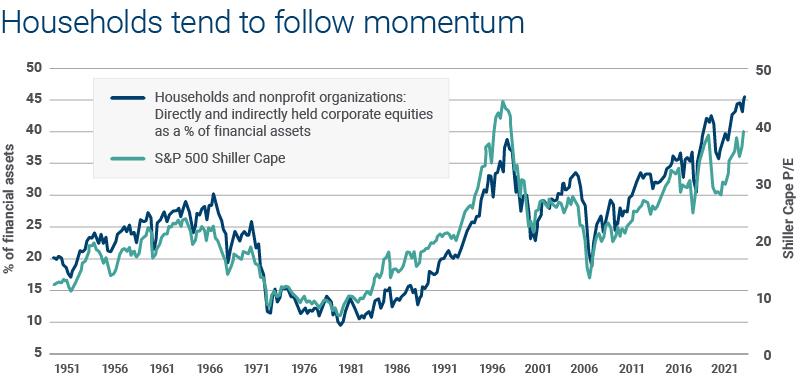

Source: Households & Nonprofit Organizations (NO): Directly and Indirectly Held Corporate Equities as % of Financial Assets sourced from Board of Governors of the Federal Reserve System (US), retrieved from Federal Reserve Bank of St. Louis (FRED) on Oct. 14, 2025. S&P 500 Shiller Cape sourced from FactSet, Robert Shiller, Yale University Department of Economics. US Shiller Cape ratio is the price-to-earnings ratio based on average inflation-adjusted earnings from the previous 10 years. Quarterly data from Dec. 31, 1951 to June 30, 2025 (Households & Nonprofit Organizations (NO): Directly and Indirectly Held Corporate Equities as % of Financial Assets) and Sept. 30, 2025 (S&P 500 Shiller Cape).

What the past may tell us about the future

Currently, households hold a high percentage of their wealth in corporate equities. This high allocation to stocks suggests that equity market returns over the next decade may be quite different from those in the past.

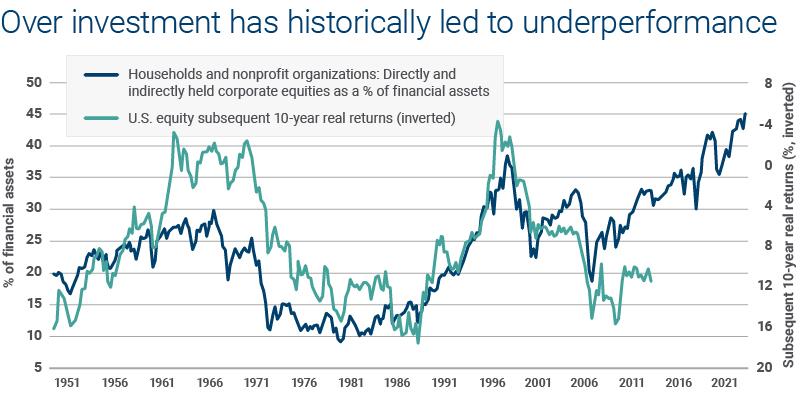

Source: Households & Nonprofit Organizations (NO): Directly and Indirectly Held Corporate Equities as % of Financial Assets sourced from Board of Governors of the Federal Reserve System (US), retrieved from Federal Reserve Bank of St. Louis (FRED) On Oct.14, 2025. US Equity Subsequent 10-year real returns sourced from Morningstar. US Equity represented by Ibbotson Associates Large Cap Stock (proxy for S&P 500). Real returns calculated by deflating index level by US Consumer Price Index. 10-year real returns are calculated using monthly data, but displayed quarterly. Returns are annualized, gross and in USD. Quarterly data from Dec. 31, 1951 to June 30, 2025. This example is shown for illustrative purposes only and is not guaranteed. Past performance is not a guarantee of future results.

Perhaps a more appropriate way to think about future returns is through the lens of the capital cycle. When capital is under- or over-allocated versus expected utility, returns get distorted. Asset price volatility occurs when new data disproves prior return assumptions.

While recent corporate earnings have been strong, current stock prices likely already reflect those high expectations. At the same time, credit losses have emerged, many consumer-facing companies have cited affordability issues and weakness was seen among businesses threatened by AI, such as software businesses with seat-based licensing models.

Beyond the quarterly results, we continue to worry about stretched valuations, the sustainability of elevated profit margins in the face of higher interest rates and a resurgence in capital expenditures to defend long-held economic moats against AI-fueled competitors.

How investors can navigate a lower-return environment

Overall, we believe that the investors face the prospects of a more difficult operating environment for businesses, coupled with the challenges of high equity valuations and the likelihood of lower returns as the capital cycle ebbs.

To this end, investors may want to consider the following approaches:

Rigorous security selection: This involves avoiding businesses with growing obsolescence risk while allocating capital to companies that are able to use new technology to their advantage and sustain returns.

Professional discipline: The advantage of professional investors lies in their training and discipline to combat more than 4 billion years of evolution. They are taught to run toward things that “taste bad” — underpriced assets with negative recent returns — and run away from things that “taste good” — inflated assets with strong trailing returns. We refer to this as Time Horizon Arbitrage: a disciplined approach of exploiting the short-term, emotionally driven behaviors of others for long-term gain.

Get long-term guidance for changing markets

Your Ameriprise financial advisor is here to help you navigate every market cycle and avoid emotional investing decisions. From building a portfolio that reflects your goals and risk tolerance to offering steady, long-term guidance, they can help you stay focused and invested when markets feel uncertain.